The Moroccan Agency for Solar Energy and the Moroccan Solar Plan

- Oct 10, 2013

- 4 min read

This case study outlines the key role of the ‘Moroccan Agency for Solar Energy’ (MASEN) in enabling the country to attract private investment for its first large concentrated solar power installation as part of a wider energy and industrial development strategy.

Context

In recent years Morocco has imported 95% of its energy as fossil fuels, providing subsidies on these fuels at a cost between US$1-4 billion per year. With a growing population, rising living standards and increasing power demand from cities and energy intensive industry, key priorities are to increase and diversify the energy supply, and manage public costs (Nabil, 2013).

With natural resources for wind, hydro and solar, renewables are recognized as offering the opportunity to reduce dependence on imports while generating employment and cutting greenhouse gas emission, with the potential for future green electricity exports to Europe (Dominguez, 2013). Concentrated solar power (CSP) is seen as a particularly important opportunity because of its ability for storage and the chance build up a local supply industry in an emerging industry (African Development Bank, 2013).

Objective

The government set a goal of reaching 42% of installed capacity (or 6,000 MW) from renewable energy (hydro, wind and solar) by 2020, whilst doubling overall capacity (Norton Rose Fulbright, 2012). Through the Morocco Solar Plan (MSP) it aims to install 2,000 MW of solar capacity by 2020, contributing around 14% of the energy mix in the country’s electricity supply. The plan calls for the construction of 5 solar complexes in requiring an estimated investment of $9 billion. (African Development Bank, 2012) .

Challenge

CSP is currently more expensive than fossil fuel based energy generation (even if fossil fuel subsidies are removed), thus requiring a blend of public subsidy and risk mitigation instruments to attract private investors.

The government’s previous involvement in the development of CSP had been limited to a 20MW plant (Ain Beni Mathar) developed by the national utility office (l'Office National de l'Electricité – ONE), while existing privately financed CSP instillations were small scale and built for private use. The MSP (including Ourzazate 1, 2 and 3) are much larger developments which would place a large financial burden on the existing energy and fiscal system (see Table 1) (CSP World)

A number of donors were already active or had indicated their interest to support a catalytic large scale renewables program in Morocco, for example through policy based lending for reforms, concessional finance to buy down incremental costs, carbon finance, advisory services and infrastructure finance (CTF, 2011), however this created a challenge of coordination, and additional complexity for private investors.

A new financing architecture was therefore needed to be developed which would blend domestic public funding with funding from international financial instrudcments (IFIs) whilst effectively aligning risks between the public and private sector partners.

In the longer term it is hoped that such early publicly supported projects will enable the technology to mature so that projects can be financed by investors and local banks, as has been experience with the longer established wind industry in Morocco (Nabil, 2013).

Approach

The government established The Moroccan Agency for Solar Energy (MASEN) in 2010 as the vehicle for mobilizing and blending resources and allocating risks to key players. It is a limited company which is 25% owned by the Government of Morocco, ONE, the Hassan II Fund1 for economic and social development, and the Société d'Investissements Energétiques (SIE)2 (Moroccan Agency For Solar Energy). The public investment is recorded as ‘equity capital and equipment subsidies’ in the General State Budget, while MASEN itself is an extra-budget entity. (Ministere de l'Economie et des Finances, 2013)

MASEN is responsible for feasibility assessment, design, development, and financing of solar projects in Morocco, along with contributing to expertise and research in the solar industry (Moroccan Agency For Solar Energy). Its aims are both to develop energy but also to support the development of a new industrial sector in Morocco through training, capacity building, and research and development (R&D) (Nabil, 2013) .

The first project to be developed using this model was Ouarzazate 1. Bids were invited to develop a Solar Power Company (SPC) to operate the plant on a ‘build, own, operate and transfer’ basis, supported by a 25 year fixed term Power Purchasing Agreement (PPA) between MASEN and the SPC. ONE is required to buy all energy from MASEN at grid price through a second PPA. The Moroccan government pays MASEN the difference between the two contracts. This arrangement guarantees a revenue stream for the SPC that is shielded from the volatility of energy prices. It is underpinned by a US$200 million contingency loan facility from the World Bank to the Moroccan government, which mitigates against public funding shortfall risk.

MASEN plays the role both of contract holder in the two power purchase agreements and as an equity partner in the SPC along with the winning bidders. This is governed by a shareholder agreement which includes a put option which allows MASEN to sell back its share if the private partner defaults on specified construction or performance obligations.

MASEN also acts as a consolidator of concessional loans provided by the Clean Technology Fund (CTF), African Development Bank (AfDB), the World Bank (WB), and the European Investment Bank (EIB) which reduce the cost of capital for the SPC, and lower the overall cost of energy generated. MASEN blends the terms of the IFI loans and offers a single financing package as part of the development and bidding process. (Falconer & Frisari, 2012a). Critically this ensures adequate financing as part of the tender offer to the SPC, giving potential private investors clear information on the debt package of the project, and ensuring that the lower cost of capital is reflected in the bid price (Falconer & Frisari, 2012a).

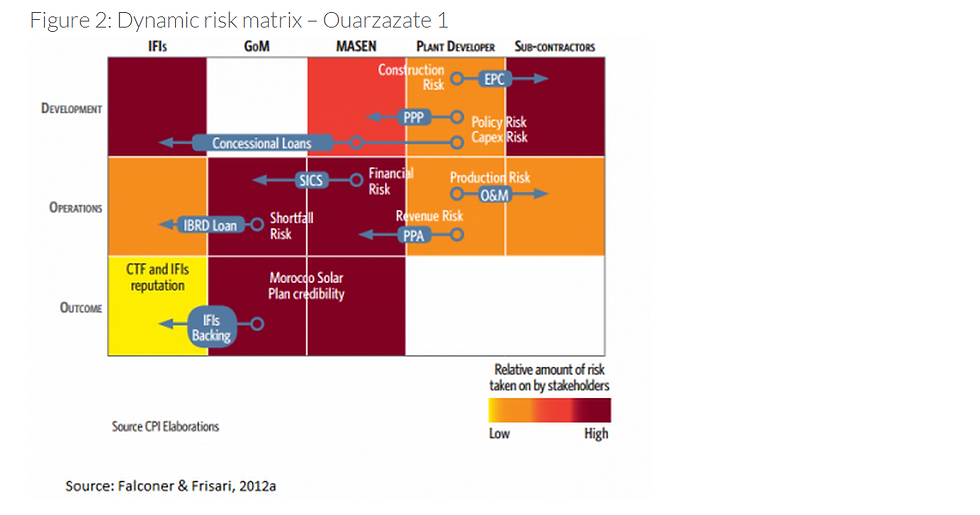

These combined measures are designed to allocate risks across investors as shown below in order to make the deal viable, while incentivizing performance (see Figure 2).

Comments